Virtual CFO

ECLGS 5.0: How MSMEs Can Unlock Collateral-Free Working Capital in 2026

In short

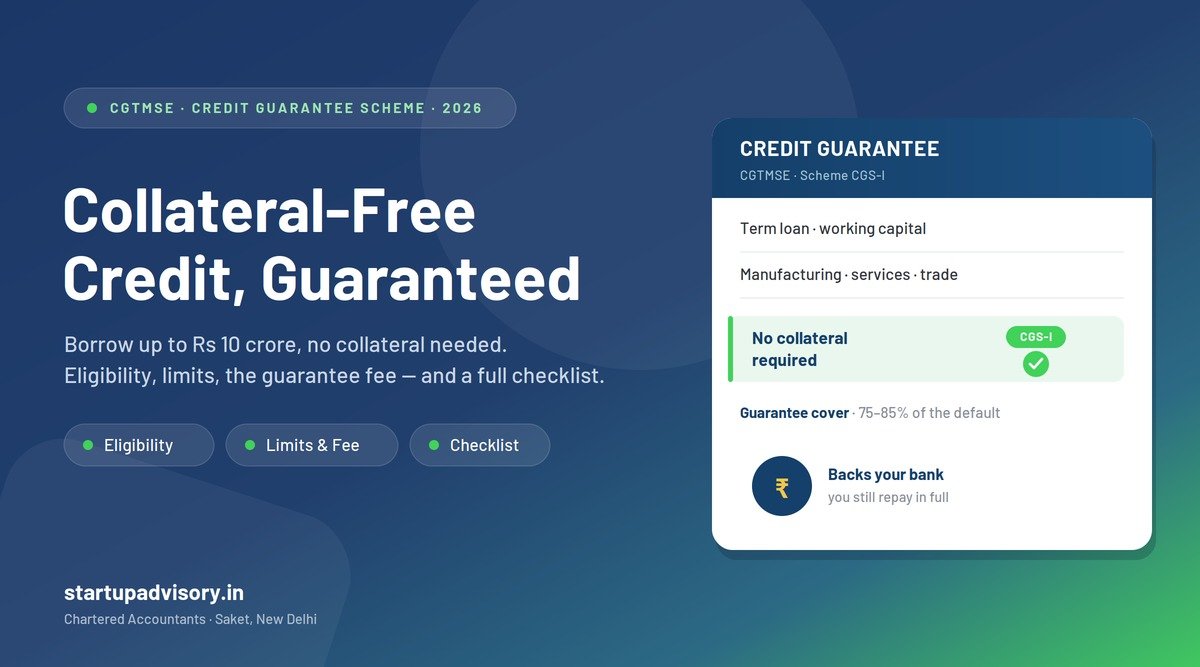

On 5 May 2026 the Union Cabinet approved ECLGS 5.0 — the fifth round of the Emergency Credit Line Guarantee Scheme — to cushion businesses against the liquidity shock from the West Asia crisis (higher fuel costs, disrupted supply chains and trade finance). It gives existing borrowers collateral-free additional working capital of up to 20% of their peak cash-credit/overdraft usage in Q4 FY 2025-26 (Jan–Mar 2026), capped at ₹100 crore, with a 100% government guarantee for MSMEs, interest capped at 9% p.a., a 5-year tenure with a 1-year moratorium, and zero guarantee, processing or prepayment fees. You apply only through the Jan Samarth portal. It runs until 31 March 2027 or until the ₹2.55 lakh crore corpus is exhausted.

If your business has felt the squeeze from rising input and fuel costs over the last few months, ECLGS 5.0 is the most borrower-friendly working-capital line available right now. This guide explains exactly who can benefit, how much you can get, when to act, and how to apply on the Jan Samarth portal — the way we walk our own clients through it.

What ECLGS 5.0 is, and why it exists now

The Emergency Credit Line Guarantee Scheme was first launched in 2020 during the pandemic. The mechanism is simple: instead of the government lending money directly, the National Credit Guarantee Trustee Company (NCGTC) guarantees the loan your bank gives you. Because the lender's risk is covered, it can extend extra credit without asking for fresh collateral.

ECLGS 5.0 revives that playbook for a new reason. The West Asia conflict has pushed up fuel and freight costs and disrupted supply chains and trade routes, straining the cash flow of thousands of businesses. The scheme channels an additional ₹2.55 lakh crore of credit into the economy to keep otherwise-healthy businesses liquid.

Key terms at a glance

| Feature | What you get |

|---|---|

| Who guarantees it | NCGTC (Government of India) — 100% cover for MSMEs, 90% for non-MSMEs & airlines |

| Loan amount (MSME / non-MSME) | Up to 20% of peak working capital used in Q4 FY 2025-26, capped at ₹100 crore |

| Collateral | None — no additional security required |

| Interest rate | Capped at 9% p.a. (EBLR/MCLR + 0.75%) |

| Tenure | 5 years, including a 1-year moratorium on principal |

| Fees | Nil guarantee fee, nil processing fee, nil margin, nil prepayment penalty |

| Where to apply | Jan Samarth portal only (jansamarth.in) |

| Open until | 31 March 2027, or until ₹2.55 lakh crore is sanctioned — whichever is earlier |

Who can benefit (and who can't)

ECLGS 5.0 is a top-up on an existing facility, not a fresh loan for new borrowers. You are eligible if:

- You are an MSME or a non-MSME business (or a scheduled passenger airline) with a fund-based working capital limit — a cash credit (CC) or overdraft (OD) account — as on 31 March 2026.

- That account was Standard (not an NPA) as on 31 March 2026. Accounts with only minor stress (classified SMA-1) are still eligible — if yours had small delays, ask your branch specifically.

You are not eligible if:

- You have no existing working capital limit — the scheme tops up what you already have, so a brand-new borrower cannot use it as a first loan.

- Your account had already slipped to SMA-2 or NPA on the cut-off date, or your sector sits on NCGTC's exclusion list.

MSMEs get the best deal — a full 100% guarantee. If you run a business but have never formalised your MSME status, getting your Udyam (MSME) registration in place first is worth doing, as it unlocks the higher guarantee cover.

How much can you actually get?

The amount is tied to how much of your working capital you used — not your sanctioned limit — during the last quarter of FY 2025-26 (1 January to 31 March 2026):

Additional credit = up to 20% of your peak CC/OD utilisation in Q4 FY 2025-26 (capped at ₹100 crore).

Worked example: if the highest balance you drew on your cash credit or overdraft between January and March 2026 was ₹2 crore, you can apply for up to ₹40 lakh of additional credit. Your bank reads this figure straight from your account statements, so you don't need to calculate it precisely — but knowing the formula helps you set realistic expectations before you apply.

When to act

Two dates matter. The scheme is open until 31 March 2027, but it also stops the moment the ₹2.55 lakh crore corpus is fully sanctioned. Government guarantee schemes with a fixed pool have historically been claimed faster than the calendar deadline. If you are eligible and the cash would genuinely help, treat the corpus — not the date — as your real deadline, and get your paperwork ready now.

How to apply on the Jan Samarth portal — step by step

For ECLGS 5.0, applications are routed mandatorily through the Jan Samarth portal at jansamarth.in. It is a free, government-run platform that connects you to credit-linked schemes and forwards your application to your existing lender. Here is the practical flow:

- Step 1 — Register & check eligibility. Create an account on jansamarth.in and complete the short eligibility questionnaire for the business-loan / ECLGS category.

- Step 2 — Fill your business profile. Basic details of the entity — name, constitution, sector and your existing bank / working-capital account.

- Step 3 — Upload your documents. Keep these ready before you start (incomplete files are the single biggest cause of delays):

- Your business profile / KYC

- Updated GST registration certificate (and recent GST returns)

- Your Udyam / MSME certificate

- Turnover figures / latest financials

- Your peak OD or CC utilisation during the last quarter of FY 2025-26 (your bank statements for Jan–Mar 2026 show this)

- Step 4 — State how much you need. Enter the amount you want, keeping it within the 20% cap calculated above.

- Step 5 — Submit & track. The portal routes your request to your existing lender (the bank or NBFC where your working-capital account sits). They verify the numbers, NCGTC provides the guarantee, and the additional credit is disbursed — with no fresh collateral demanded.

You do not need to switch banks: ECLGS 5.0 is disbursed through your current Member Lending Institution.

A Virtual CFO's tips before you apply

- Reconcile your books first. The whole application hinges on clean, accurate financials and a verifiable Q4 utilisation figure. Messy books slow everything down — sort your bookkeeping before you apply.

- Borrow to a purpose, not just because it's cheap. A 9% collateral-free line is attractive, but it is still debt. Map it to a specific need — bridging a receivables gap, funding an order, smoothing seasonal cash flow — and into a cash-flow plan with a clear repayment path. The 1-year moratorium helps, but the principal still falls due.

- Check your MSME status. The 100% guarantee (vs 90%) makes Udyam registration worth completing first if you qualify.

- Confirm the exact terms with your lender. Caps, eligibility and rates follow the official NCGTC guidelines, but individual banks apply them within their own credit policy — always confirm specifics with your branch.

How Startup Advisory helps

Deciding whether to take ECLGS 5.0, how much to draw, and fitting it into a repayment plan is exactly the kind of financial-leadership call a Virtual CFO exists for. Our Saket team helps Delhi NCR businesses get their books and documents application-ready, work out the right amount to borrow, and use the line productively rather than just because it's available. If you'd like a second opinion before you apply, talk to us.

This article is general information, not financial or legal advice. Scheme terms are set by the Government of India and your lender and can change — verify the current details on jansamarth.in or with your bank before acting.

How Startup Advisory Can Help

Startup Advisory is a CA-led firm in Saket, New Delhi that helps MSMEs across Delhi NCR become eligible for — and ready to use — schemes like ECLGS and CGTMSE working-capital support. Lenders want a registered MSME with clean books, and that is what we set up:

- MSME / Udyam registration so you qualify for priority lending and credit-guarantee cover.

- Loan-ready financials and projections through our Virtual CFO service.

- Clean, lender-ready bookkeeping that strengthens your application.

- A named Chartered Accountant who helps you present a fundable case to the bank.

Call 9311972982 or book a free consultation to get working-capital ready.