Tax & ITR

ITR Filing in 2026 (AY 2026-27): Forms, New Rules & 20 FAQs

In short

For FY 2025-26 (AY 2026-27), the CBDT notified every ITR form (ITR-1 to ITR-7) on 30 March 2026, so the filing window is already open. The new tax regime is the default, with zero tax up to Rs 12 lakh (about Rs 12.75 lakh for salaried, after the Rs 75,000 standard deduction). ITR-1 now covers up to two house properties. Key deadlines: 31 July 2026 (ITR-1/2), 31 August 2026 (non-audit ITR-3/4) and 31 October 2026 (audit). Your return is still filed under the old Income Tax Act, 1961 — the new Act applies from next year.

This is not a routine filing season. The forms arrived early, the new regime is firmly the default, and India is running two tax laws side by side. Get the basics right and AY 2026-27 is one of the smoothest filing years yet. Here is everything Delhi NCR taxpayers need before they hit submit.

What's new for ITR filing in 2026

- Forms notified early. All forms (ITR-1 to ITR-7, plus ITR-V and ITR-U) were notified on 30 March 2026, with a corrigendum on 10 April 2026 fixing minor schedules. The utilities are already live on incometax.gov.in.

- ITR-1 now covers two house properties. Salaried owners of a second home no longer need the more complex ITR-2 — provided total income stays within Rs 50 lakh.

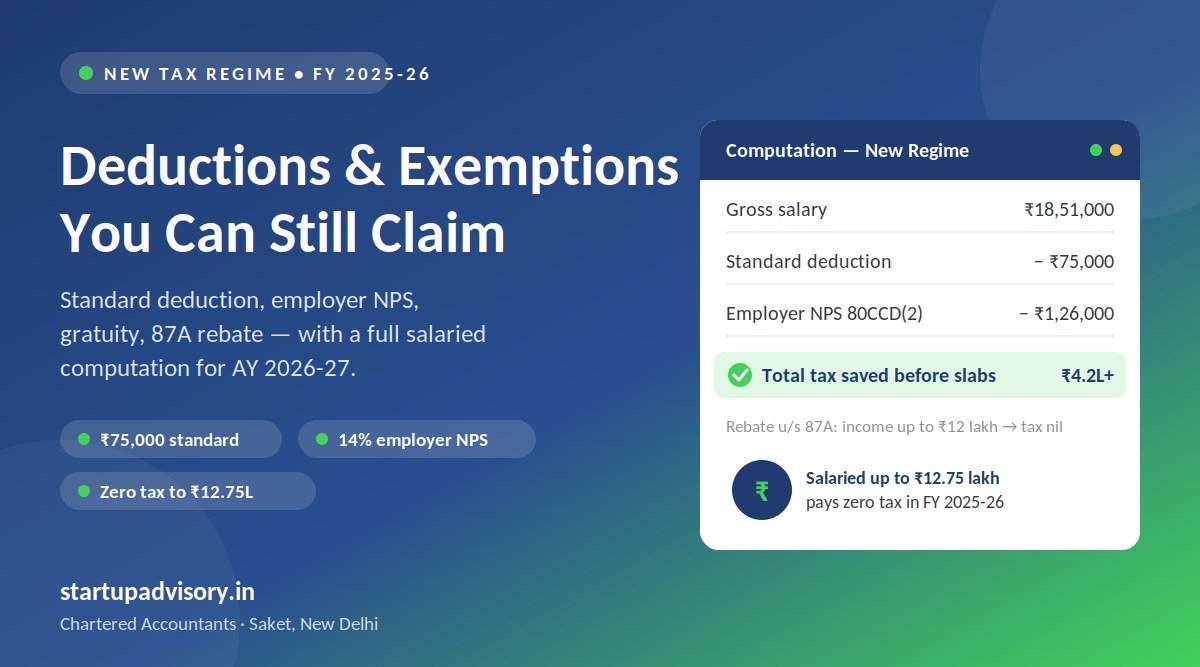

- Zero tax up to Rs 12 lakh. The enhanced Section 87A rebate (up to Rs 60,000) makes income up to Rs 12 lakh tax-free under the new regime — about Rs 12.75 lakh once you add the standard deduction.

- New regime is the default. You are taxed under it unless you actively opt for the old regime.

- Staggered deadlines stay. Non-audit ITR-3/ITR-4 filers now have until 31 August — a permanent change, not a one-off extension.

- Longer to revise. The revised-return deadline has moved to 31 March 2027.

- Old law still applies. Despite the Income Tax Act 2025 being in force from 1 April 2026, AY 2026-27 is governed by the old Income Tax Act, 1961.

Which ITR form should you use for AY 2026-27?

Picking the right form is the single most common place filers go wrong. Use this as a quick map:

| Form | Who files it |

|---|---|

| ITR-1 (Sahaj) | Resident individuals with total income up to Rs 50 lakh — salary/pension, up to two house properties and other sources (no business income) |

| ITR-2 | Individuals/HUFs with capital gains, more than two properties, or foreign income/assets — but no business income |

| ITR-3 | Individuals/HUFs with income from business or profession |

| ITR-4 (Sugam) | Presumptive taxation under Sections 44AD/44ADA/44AE, total income up to Rs 50 lakh |

| ITR-5 | Firms, LLPs, AOPs and BOIs |

| ITR-6 | Companies (other than those claiming Section 11 exemption) |

| ITR-7 | Trusts, charitable institutions and political parties |

Freelancers and consultants usually file ITR-4 or ITR-3 — see our ITR guide for freelancers.

The headline change: zero tax up to Rs 12 lakh

The biggest story this season is the revamped new-regime structure that took effect for FY 2025-26. The basic exemption rose to Rs 4 lakh, and the Section 87A rebate was raised so that resident individuals with taxable income up to Rs 12 lakh pay no tax at all. Here are the new-regime slabs:

| Income slab (new regime) | Rate |

|---|---|

| Up to Rs 4,00,000 | Nil |

| Rs 4,00,001 – Rs 8,00,000 | 5% |

| Rs 8,00,001 – Rs 12,00,000 | 10% |

| Rs 12,00,001 – Rs 16,00,000 | 15% |

| Rs 16,00,001 – Rs 20,00,000 | 20% |

| Rs 20,00,001 – Rs 24,00,000 | 25% |

| Above Rs 24,00,000 | 30% |

A salaried person with gross salary up to about Rs 12.75 lakh pays nothing under the new regime once the Rs 75,000 standard deduction is applied. Just above Rs 12 lakh, marginal relief keeps the extra tax from exceeding the extra income. The old regime keeps its full menu of deductions (80C, 80D, HRA, home-loan interest) but steeper slabs — so it only wins if your deductions are large. Not sure which fits you? Read New vs Old Tax Regime in 2026.

The new regime is now the default — and the late-filing trap

Because the new regime applies automatically, the old regime is now an active choice you must make on time:

- Salaried / non-business taxpayers: tick the "opting out of the new regime" option directly in the ITR each year.

- Business / professional income: file Form 10-IEA before the due date to opt for the old regime.

The trap: if you miss your due date and file a belated return, you generally lose the right to the old regime entirely. You are then taxed under the new regime and forfeit 80C, 80D, HRA and home-loan-interest benefits. For anyone relying on those deductions, filing on time is not just good hygiene — it directly protects your tax bill.

Deadlines that matter

| Taxpayer / form | Due date (AY 2026-27) |

|---|---|

| Individuals — ITR-1 / ITR-2 (no audit) | 31 July 2026 |

| Non-audit business / profession — ITR-3 / ITR-4 | 31 August 2026 |

| Audit cases | 31 October 2026 |

| Belated return | 31 December 2026 |

| Revised return | 31 March 2027 |

For the full breakdown, including the tax-audit-report and transfer-pricing dates and the exact penalties, see our ITR due dates for AY 2026-27 guide.

Why you still file under the old Income Tax Act, 1961

This is the point that has confused taxpayers most this year. The Income Tax Act 2025 came into force on 1 April 2026 — but your AY 2026-27 return covers income earned between 1 April 2025 and 31 March 2026, a period that belongs to the old law. So you file under the Income Tax Act, 1961, using familiar sections like 80C, 80D, 24(b) and 87A. The new Act first applies to income of FY 2026-27 (the new "Tax Year"), with returns due in 2027. For more, read Income Tax Act 2025: what changes.

Documents to gather before you file

- Form 16 from your employer (salary TDS certificate)

- Your AIS and Form 26AS — reconcile them against actual income and TDS

- Bank and fixed-deposit interest certificates; PPF/NSC statements

- Capital-gains statements (broker/AMC) if you sold shares, mutual funds or property

- Rent receipts, home-loan interest certificate and Section 80 proofs (if using the old regime)

File early, stress less

With forms and pre-filled data already live, there is no reason to wait for July. Early filing means faster refunds, time to fix AIS mismatches, and no last-week portal crush. Our Saket team handles ITR filing and tax advisory for salaried individuals, founders, freelancers and businesses across Delhi NCR.

This is general information, not tax advice. Dates can be extended by the CBDT and the right answer depends on your individual situation — confirm with a qualified professional before filing.

How Startup Advisory Can Help

Startup Advisory is a CA-led firm in Saket, New Delhi that handles income tax filing for individuals, freelancers and businesses across Delhi NCR. If you would rather not decode forms, regimes and deadlines, our Chartered Accountants take the whole return off your plate:

- End-to-end ITR filing and tax advisory — the right ITR form, every eligible deduction, filed on time.

- Capital-gains, foreign-income and multiple-employer situations handled correctly.

- Year-round bookkeeping and TDS support so your numbers are ready before the due date.

- A named CA who reviews your return and answers any notice that follows.

Call 9311972982 or book a free consultation to get your return filed correctly.