Tax & ITR

New vs Old Tax Regime in 2026: Which Should Delhi Founders & Salaried Choose?

In short

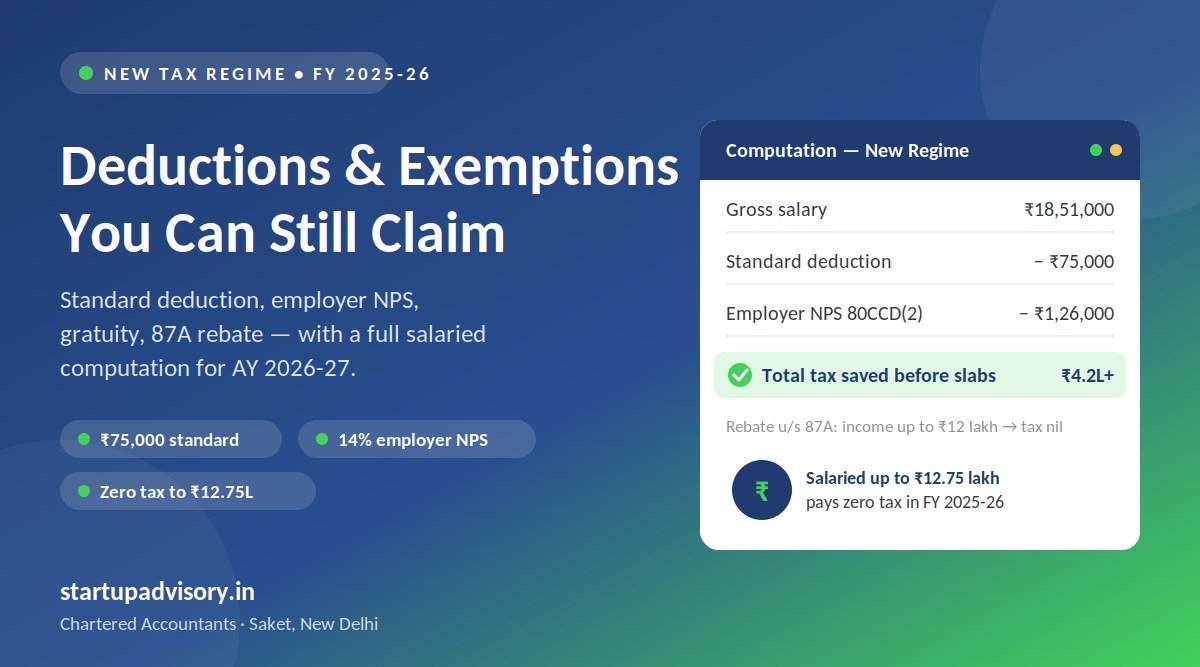

The new regime is the default and now offers zero tax up to Rs. 12 lakh of income (about Rs. 12.75 lakh for salaried, after the Rs. 75,000 standard deduction) thanks to the enhanced 87A rebate. It has lower rates but few deductions. The old regime still allows 80C, 80D, HRA and home-loan interest — so it can win if you have large deductions. Budget 2026 left both unchanged for FY 2026-27. The right pick depends entirely on your numbers.

Since Budget 2025 made the new regime far more attractive, most people are better off there — but not everyone. Here's a clear comparison so you can decide.

New regime slabs (FY 2025-26 & FY 2026-27)

| Income slab | Rate |

|---|---|

| Up to Rs. 4,00,000 | Nil |

| Rs. 4,00,001 – 8,00,000 | 5% |

| Rs. 8,00,001 – 12,00,000 | 10% |

| Rs. 12,00,001 – 16,00,000 | 15% |

| Rs. 16,00,001 – 20,00,000 | 20% |

| Rs. 20,00,001 – 24,00,000 | 25% |

| Above Rs. 24,00,000 | 30% |

With the Section 87A rebate, a resident with taxable income up to Rs. 12 lakh pays no tax. Salaried individuals get a Rs. 75,000 standard deduction, effectively extending this to about Rs. 12.75 lakh of gross salary. Budget 2026 made no changes, so these apply for FY 2026-27 too.

What the new regime gives up

Lower rates come at a cost: most popular deductions and exemptions are not available under the new regime — including 80C (investments), 80D (health insurance), HRA, and many others (the standard deduction for salaried remains).

Where the old regime still wins

If you claim substantial deductions, the old regime can produce a lower tax bill. It's worth comparing if you have:

- Full 80C (Rs. 1.5 lakh) via PF, ELSS, insurance, etc.

- 80D health-insurance premiums

- Significant HRA (renters in Delhi NCR often do)

- Home-loan interest deduction

How to decide

Add up your deductions

Total your likely 80C, 80D, HRA, home-loan interest and others.

Compute tax both ways

Calculate your liability under each regime for your income level.

Pick the lower one

Choose the regime that gives you the smaller bill — and remember the new one is the default.

Rule of thumb

If your deductions are modest, the new regime almost always wins — especially with zero tax up to Rs. 12 lakh. If you're a heavy saver with a home loan and high rent, run the old-regime numbers before deciding. Our Saket team will compute both and file the optimal one for you — see ITR Advisory. For founders, also see tax planning for startups.

General information, not tax advice. Slabs, rebates and conditions are set by law and can change; confirm for your situation.

How Startup Advisory Can Help

Startup Advisory is a CA-led firm in Saket, New Delhi that files income tax returns for salaried individuals, professionals and businesses across Delhi NCR. Instead of guessing which regime is cheaper, let our Chartered Accountants run the numbers and file the one that genuinely saves you the most:

- A side-by-side old-vs-new regime computation for your exact income and deductions.

- Accurate ITR filing and tax advisory with every eligible deduction claimed.

- Year-round bookkeeping and TDS support so filing season is never a scramble.

- A named CA who reviews your return — not a self-serve portal.

Call 9311972982 or book a free consultation and we will file the regime that costs you less.