Tax & ITR

Income Tax Act 2025: What Changes for Delhi Taxpayers from April 2026

In short

India has a new tax law. The Income Tax Act 2025 takes effect from 1 April 2026, replacing the decades-old 1961 Act. It's mainly a simplification and restructuring — clearer language, fewer cross-references, and a single "Tax Year" replacing the confusing "Previous Year / Assessment Year" pair. It applies from FY 2026-27; your AY 2026-27 return (income up to 31 March 2026) still follows the old 1961 rules. Rates are set by the annual Budget, which kept new-regime slabs unchanged.

For the first time in over six decades, India has rewritten its core income-tax law. Here's what Delhi taxpayers and businesses actually need to know — without the legalese.

What is the Income Tax Act 2025?

It's a comprehensive replacement for the Income Tax Act 1961, designed to make the law simpler and easier to read — shorter sections, plainer language, and fewer tangled cross-references. The substance of how income is taxed largely carries over; the goal is clarity, not a rate revolution.

When does it apply?

- The new Act is effective from 1 April 2026

- It applies from the financial year 2026-27 onwards

- Your return for AY 2026-27 (income earned up to 31 March 2026) is still governed by the 1961 Act

So this filing season runs on the old rules; the new Act shapes how you'll think about tax from next year.

The biggest practical change: "Tax Year"

The old law used two overlapping terms — "Previous Year" (when you earn) and "Assessment Year" (when you're assessed) — which confused countless taxpayers. The new Act replaces them with a single "Tax Year", aligning the language with how people actually think about their income.

What stays the same

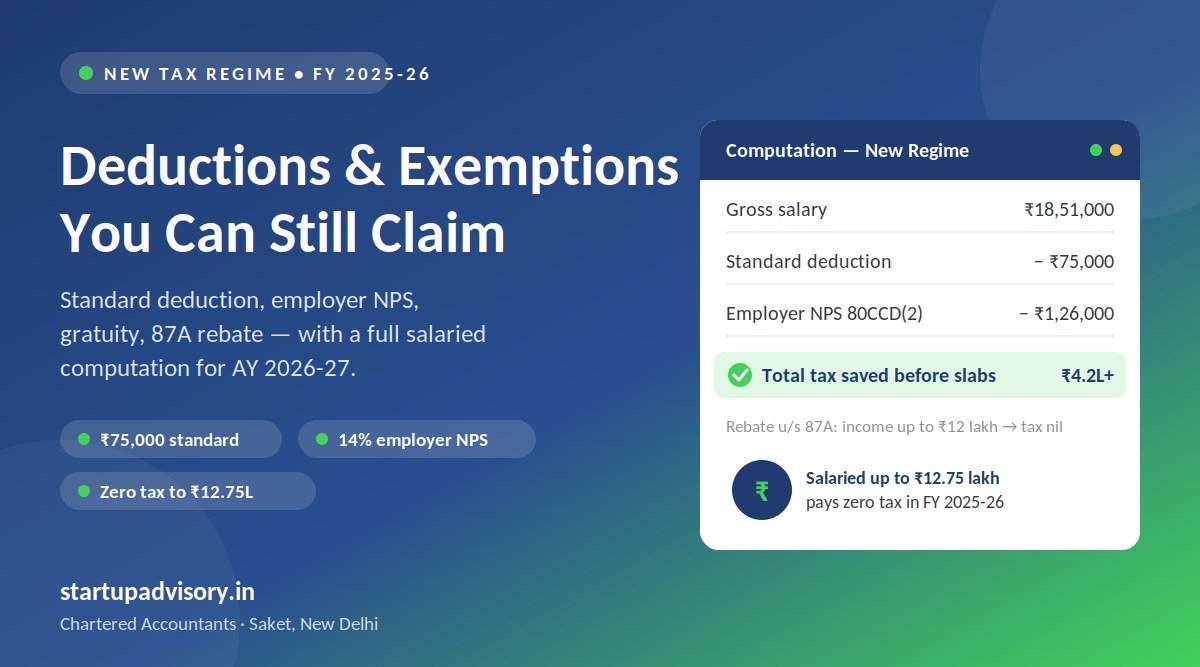

- Tax rates and slabs are still set by the annual Finance Act; Budget 2026 kept the new-regime slabs unchanged for FY 2026-27 (see new vs old regime)

- Core concepts — heads of income, deductions, TDS, advance tax — broadly continue

- Late-filing fees and similar provisions are carried into the new Act

What businesses should do

Keep records current

Maintain clean books and track income, TDS and advance tax under the new framework from April 2026.

Map old to new

Familiar sections get renumbered; an advisor can map your usual provisions to the new Act.

Review processes

Update accounting software settings, templates and compliance checklists for the new terminology and references.

The bottom line

For most Delhi taxpayers, the Income Tax Act 2025 means a clearer law rather than a bigger bill. The transition is mostly about terminology and references — but getting those right keeps compliance smooth. Our Saket team guides individuals and businesses through it as part of ITR & tax advisory.

General information, not tax advice. Provisions are subject to rules and notifications under the new Act; confirm specifics for your situation.

How Startup Advisory Can Help

Startup Advisory is a CA-led firm in Saket, New Delhi that helps individuals and businesses across Delhi NCR make sense of the new Income-tax Act, 2025 and apply it correctly. Rules have changed — we make sure your filing reflects them and that you do not pay more than you owe:

- ITR filing and tax advisory aligned with the latest Act, slabs and deduction rules.

- A review of how the changes affect your specific income and entity type.

- Ongoing bookkeeping so your records already match the new requirements.

- A named CA who tracks every amendment so you do not have to.

Call 9311972982 or book a free consultation to file confidently under the new law.