Tax & ITR

Tax Planning for Startups & Founders in Delhi NCR: Legitimate Ways to Save in 2026

In short

Legitimate tax planning — not evasion — can save founders and startups a lot. The big levers: claim the Section 80-IAC tax holiday if you're an eligible DPIIT startup, choose the optimal regime, structure founder salary and reimbursements efficiently, claim every genuine business expense, time income and spending sensibly, and plan from day one. All within the law, and far more effective than a year-end scramble.

Tax planning means using the law's own provisions to pay no more than you owe — entirely legal, and something every founder should do deliberately. Here are the highest-impact moves for Delhi NCR startups in 2026.

1. Claim the 80-IAC tax holiday

For eligible DPIIT-recognised startups, Section 80-IAC offers a 100% deduction on profits for three consecutive years within the first ten — now open to startups incorporated before 1 April 2030. It's usually the single biggest saving available. See our 80-IAC guide and DPIIT registration service.

2. Pick the right structure early

Your entity affects how you're taxed. The right choice from day one avoids costly restructuring later — compare options in Pvt Ltd vs LLP vs OPC.

3. Choose the optimal tax regime

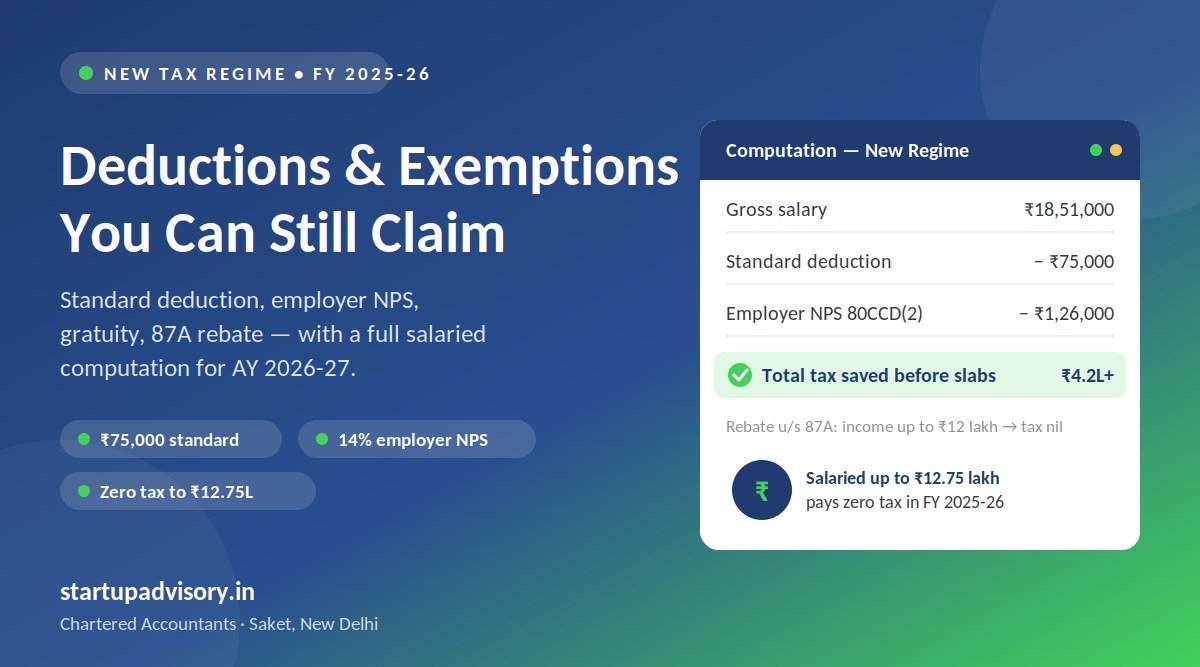

For founders drawing a salary, the new regime's zero tax up to Rs. 12 lakh is powerful — but heavy savers may still benefit from the old regime. Compute both: see new vs old regime.

4. Structure founder salary & reimbursements

How you pay yourself matters. A sensible mix of salary and legitimate, well-documented reimbursements (and, where relevant, dividends) can be more tax-efficient than a single large salary — structured correctly and compliantly.

5. Claim every genuine business expense

Many startups overpay simply by not capturing deductible costs — software, equipment, rent, travel, professional fees. Clean bookkeeping ensures nothing eligible is missed.

6. Time income and spending

Where you have flexibility, timing planned expenses or capital purchases within the right financial year can optimise your tax position — a classic, legitimate planning tool.

7. Use available deductions and exemptions

Under the old regime, 80C, 80D, HRA and home-loan interest still apply. Even under the new regime, the standard deduction and certain employer contributions help. Match deductions to whichever regime you choose.

Planning ≠ evasion

To be clear: tax planning uses the law to reduce tax legally; tax evasion is illegal concealment. Everything above is legitimate — and exactly what a good advisor helps you do. The earlier you start, the more you save. Our Saket team builds year-round tax plans for founders and startups across Delhi NCR — see ITR & Tax Advisory, often alongside a Virtual CFO.

General information, not tax advice. Provisions and limits are set by law and can change; always plan with a qualified advisor for your specific situation.

How Startup Advisory Can Help

Startup Advisory is a CA-led firm in Saket, New Delhi that builds year-round tax plans for founders and businesses across Delhi NCR. Good tax planning is a 12-month exercise, not a March scramble — we help you keep more of what you earn, legally:

- Proactive tax planning and ITR filing across salary, business and capital-gains income.

- Virtual CFO support that aligns tax strategy with cash flow and growth.

- Startup India (DPIIT) and Section 80-IAC structuring for eligible startups.

- A named CA who plans ahead with you — not just files at the deadline.

Call 9311972982 or book a free consultation to build your tax plan for the year ahead.